6 Tips To Profiting From Interest Rate Rise

- 4 MINUTES READ

By now you most probably would have seen articles or media releases that major banks are increasing their fixed rate products which provide an indication of where the bank’s vision is heading towards. What does this mean for you as a property owner during this period of time when unpredictability is in an all time high?

Many would be worried that they are no longer able to enter the market given that interest and house prices keep rising.

The Reserve Bank Of Australia stated that for the first time in six years they are entering that target range in core inflation to 2.1% in the September quarter. The lifting of lockdowns in NSW, Victoria and the ACT have prompted signs of economic recovery sending its strongest signal that economy is ready to bounce back. In order for the actual inflation rate to remain within 2-3%, the labour market will need to generate wages growth and job opportunities that are materially higher than it is currently. The country’s Central Bank declared “a bounce back is now under way” after the Covid outbreak.

6 TIPS TO PROFITING FROM INTEREST RATE RISE

1. Increasing rent on your property to keep up with the market

Just as real estate prices change and sales markets evolve from month to month, so do rental markets. When vacancy rates are tight (sub 3%) the market is more competitive and landlords can be more choosey. When vacancies are really low (at 1% or less), this can put pressure on asking rents and allow landlords to increase their profits by pushing up the rent.

Having regular small increases in rent that are just above the Consumer Price Index will ensure that you stay ahead of inflation. For instance, an increase of 3-5% every year is generally palatable; on a home that rents for $500, it would add around $15-$25 to the weekly rent.

This not only ensures you’re earning a fair market rent, but it will also prevent your tenants from being financially overwhelmed by a sudden large rental increase, should you wait a few years to raise the rent. Overwhelmed by a sudden large rental increase, should you wait a few years to raise the rent.

Remember, as a landlord you are providing someone with a home, but you’re also (meant to be) profiting from an asset. At the end of the day your goal is to make money from your property, so while giving your tenants a discount and only doing them a huge favour, it does no favours to you and your long-term wealth.

2. Getting prepared for when interest rates rise: (not until late 2023)

The central forecast is for underlying inflation to be no higher than 2.5% at the end of 2023 and for only a gradual increase in wages growth. The RBA expects GDP growth of 3% over 2021 and 5.5% and 2.5% over the following two years. The encouraging comments about the economy will likely mean interest rates rise sooner than that 2024 scenario previously stated by the bank.

While the cash rate was left unchanged for now, the RBA has surrendered to market forces and ceased trying to keep the yield on the benchmark April 2024 to just 10 basis points, or 0.1%. However, the bank also maintained its bond buying at the $4bn a week pace until at least mid-February 2022. The decision to discontinue the yield target reflects the improvement in the economy and the earlier-than-expected progress towards the inflation target. Given that other market interest rates have moved in response to the increased likelihood of higher inflation and lower unemployment, the effectiveness of the yield target in holding down the general structure of interest rates in Australia has diminished..

3. having a cash buffer: (2-4 months)

Careful planning and preparations for when something unexpected happens require a successful property investment strategy. While the long-term benefits of property investment should far outweigh short-term costs, property investors are sometimes faced with unplanned situations that impact their immediate cash flow, which is why smart investors will always set aside a cash buffer to cover unexpected expenses.

As a guide, you should look to have two to four months of rental income on hand as a property investment buffer, as well as two to four months of personal income set aside as a personal income buffer. The risk of unexpected expenses can never be fully mitigated, property investors can deal with this risk by planning ahead and making smarter investment decisions.

As well as setting aside an emergency buffer, this means having the right professionals on hand to manage your property and take care of situations that put your rental income at risk. Most importantly, it means making the right decision when selecting a suitable property in the first place.

4. If Interest Rates Goes Up

If interest rates were to rise significantly, resulting in more investors finding themselves staring down the barrel of losing money on their property, the federal government will effectively foot part of the additional cost through negative gearing tax deductions. As housing prices continue to rocket higher, investor interest in the market is likely to continue to grow, as the allure of strong capital growth draws in more buyers.

Consistently losing money week in, week out may seem like the exact opposite of what an investor would want from an asset. But for Australian property investors, losing money in the hope of strong housing price growth has become a way of life. While higher interest rates are likely a factor in the back of the minds of many investors looking to potentially buy in this market, negative gearing provides them with a strong incentive to pull the trigger anyway.

5. Growing Job Opportunities

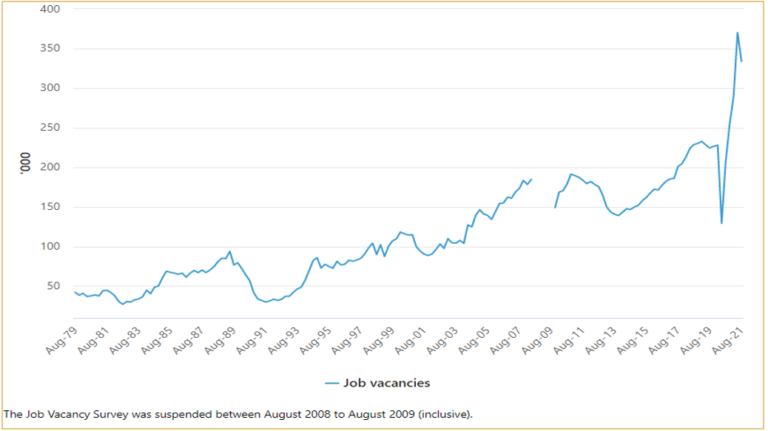

Job vacancies decreased by 9.8% (36,200 vacancies) in the three months to August 2021 (seasonally adjusted). The August vacancies reflect a point in time when many businesses were subject to restrictions, with a number of states in lockdown.

However, the level of job vacancies remained higher than they were six months ago, and were still 46.5% higher than in February 2020, prior to the start of the pandemic. The ongoing high level of vacancies reflects the pace of recovery in labour demand from the fall in May 2020, as well as a number of industries indicating labour shortages, particularly for lower paid jobs.

Employment is projected to increase in 17 of the 19 broad industries over the five years to November 2025. With more and more job opportunities, income also increase. Australian economy continuously improves this reflected from better and competitive market.

6. Hybrid Job Environment

As we adapt from “The new normal” life, this completely change how we view life as well as our job environment. Working remotely or work from home might difficult at first and many people have taken some time to get used to, but in the long run with some perks. Such as saving extra cash, working at home became advantages. As more companies are adapting with working from home with the option of visiting the office 1-2 times per week. Workers are happier as they can spend more time with family along with cutting unnecessary expenses such as dining out and transportation.

There’s also potential health benefits when working from home. With less time spent commuting, you might be able to squeeze in extra exercise, or catch up on sleep. Plus, fewer cars on the road and less disposable coffee cups being used helps our environment. Working from home, even if it’s just a few days a week, might help reduce your costs and give you a bit extra in your bank account. While you might not be able to hang out with your teammates as much, make the most of those sleep-ins (and savings!) while you can.

Your complimentary strategy session

If you have your savings and you are not sure how to invest but you want to start building your wealth, getting started in real estate can be an option as there are many opportunities to explore. Our team will work with you 1-on-1 to firstly understand your financial situation then create a tailored investment plan specifically towards your future goals. Let our experts help guide you through all those obstacles that you’ll face during your property journey by booking a Property Strategy Session with us today!